We feel investors should have an information outlet for the financial markets that is thorough, but does not require a prerequisite degree in economics. We hope this makes our commentary informative and educational for all levels of investors.

Quarter in Review

| Asset Class† | 3rd Quarter 2019 Return | Past 12 Months |

| U.S. Bonds | 2.3% | 10.3% |

| U.S. Large Cap Stocks | 1.7% | 4.3% |

| International Stocks | -1.8% | -1.2% |

| Commodities | -1.8% | -6.6% |

| U.S. Small Cap Stocks | -2.4% | -8.9% |

The stock market movements during the 3rd quarter of 2019 were much like the variable weather during that time of year. Many days were like beach days when the U.S. stock market was relatively calm and unchanged, while other days had major movements seemingly out of nowhere, like a thunderstorm rolling in with the late summer heat. This pattern has served as a reminder to not get too comfortable in this mature bull market. In the end, the S&P 500 notched a positive return for the third quarter, adding gains to what is the best start to a year through nine months since 1997. However, increased volatility for smaller U.S. companies and foreign markets that have continually lagged behind large U.S. companies have created a much less uniform landscape for stocks as a whole.

In the Headlines: Politicians and Market Perspectives

Despite the high volatility in the markets, it pales in comparison to the volatility of the political circus that is consuming the media outlets these days. It is hard to tell how the Trump impeachment proceedings will play out between now and the election next fall, but one early winner is Elizabeth Warren as her move to the top of the Democratic primary polls has coincided with the start of impeachment hearings. Warren’s position is further strengthened as impeachment will almost certainly hinder Trump’s re-election prospects and at the same time could also affect Joe Biden’s prospects if his Democratic rivals use his son’s involvement with Ukraine against his candidacy as well. All this political news is important within the context of the investment markets because while Trump and Biden are the two biggest free market proponents out of the top 5 current candidates (Bernie Sanders, Kamala Harris and Elizabeth Warren round out the five), Warren has made many campaign promises to make sweeping changes to our current economic system. The coming months should be interesting as candidates continue to strengthen and verbalize their platforms, including their thoughts on the market and plans for the future.

Looking Ahead: Stocks Not Following Previous Signs of Recession

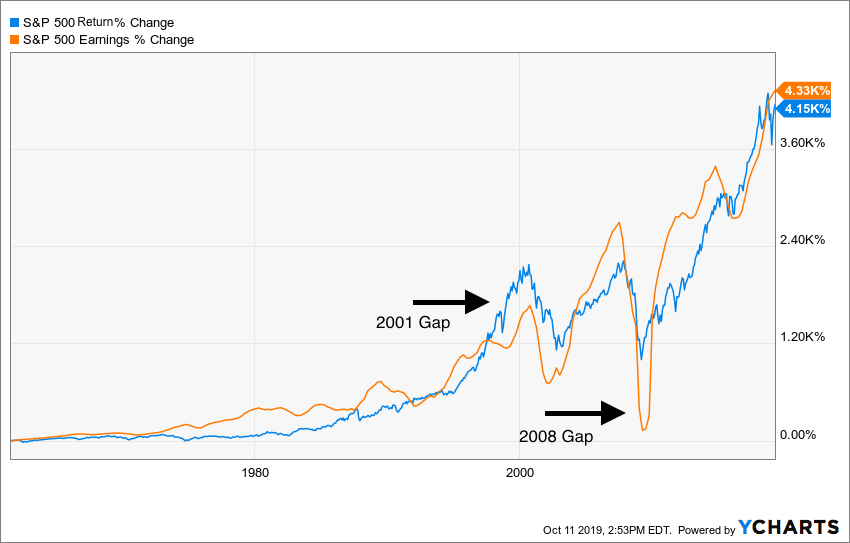

Unlike the last two most recent recessions (2001 and 2008), company earnings reflect that this market still has room to grow. This is notable because one important piece missing from a potential looming recession is a de-coupling or separation of the growth trajectories of stock returns and the underlying earnings reported by companies.

To zoom out a bit, the relationship between the return of a company (how much the stock price rises or falls) and the earnings of that company (how much money the company makes) have historically been a good yardstick to measure the desirability of that company as an investment. Indexes, such as the S&P 500, are groups of companies that make up a certain market, which in the S&P 500’s case, are 500 large U.S. companies. The makers of the indexes provide the total earnings made by all the companies within the index in order to show how well the underlying companies are performing relative to how much the index is rising or falling each day in the market.

Since market return performance and the underlying earnings of a company are independent of each other, they do not always move in tandem and tend to fluctuate depending upon many factors such as the state of the overall economy and the future outlook of individual company prospects. As a rule of thumb, the market returns are usually higher than the earnings during boom times with expectations of future growth and are typically lower entering recessions when investors question the solidity of the earnings previously produced. However, over long periods of time, the booms and busts tend to iron out and the market price and the underlying earnings move very closely together.

Getting back to how this relates to our current economy, in the past two recessions (2001 and 2008) a separation has occurred when market returns outpace the underlying earnings as the following chart shows.

In 2000, the market (in blue) continued to advance higher despite earnings (in orange) not increasing at as fast of a pace, creating a gap between the market growth and earnings growth. 2008 played out a bit differently, as the gap in returns and earnings emerged after the declines in both had already started. Looking at today’s numbers, there isn’t currently a significant gap between the market returns and the underlying earnings, as both have continued to move mostly in tandem especially for the past 3-4 years.

There is no law stipulating that this separation must occur prior to a market downturn, and just because it has not started at this current time, doesn’t mean that it won’t in the coming months. It is however, another piece of data that indicates we are in an unusual period within recent market history where typical indicators are not matching up.

IMPORTANT INFORMATION

† Indices used to represent asset classes:

U.S. Large Cap Stocks – S&P 500

U.S. Small Cap Stocks – Russell 2000

International Stocks – MSCI ACWI ex-U.S.

U.S. Bonds – Bloomberg Barclays Aggregate

The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes and represents Wilson Capital’s views based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Wilson Capital is a Registered Investment Advisor (“RIA”), registered in the state of Massachusetts. Wilson Capital provides asset management and related services for clients nationally. Wilson Capital will file and maintain all applicable licenses as required by the state securities boards and/or the Securities and Exchange Commission (“SEC”), as applicable. Wilson Capital renders individualized responses to persons in a particular state only after complying with the state’s regulatory requirements, or pursuant to an applicable state exemption or exclusion.