We feel investors should have an information outlet for the financial markets that is thorough, but does not require a prerequisite degree in economics. We hope this makes our commentary informative and educational for all levels of investors. We have also included a glossary at the end of this commentary that defines terms marked with an asterisk (*).

Quarter in Review

| Asset Class† | 4th Quarter 2017 Return | Past 12 Months |

| International Stocks | 5.0% | 27.2% |

| U.S. Large Cap Stocks | 6.6% | 21.8% |

| U.S. Small Cap Stocks | 3.3% | 14.7% |

| U.S. Bonds | 0.4% | 3.5% |

| Commodities | 4.7% | 1.7% |

2017 proved to be one of the most prolific years on record for stocks around the globe. This marks the 9th straight year with a positive annual return for the U.S. Large Company S&P 500 index and matches the record for the most consecutive years of positive returns since the index was created in 1923. Outside of the U.S., International stocks around the world joined in on the party in a big way this year by returning over 27% as a whole with Emerging Markets, a sub-sector of the international market which includes countries such as China and India, returning 37%.

The positive results continue to be predicated on accommodating Federal Reserve policies for businesses and a Republican political agenda that promotes leniency on regulations. With the unemployment rate at the lowest level in years and consumer confidence at its highest level since the year 2000, the wheels of the economy had been greased for the resulting gains.

Outlook

While equity markets have been roaring higher without taking much of a breath in the past 9 years and interest rates making the sharpest moves higher in a half decade, this is not the time to put the blinders on. There is an old saying on Wall Street that “bull markets don’t die of old age”, but rather by events that might be both sudden and unexpected. The most salient events right now are market bubbles, interest rates, and a blanket category of politics.

Market Bubbles

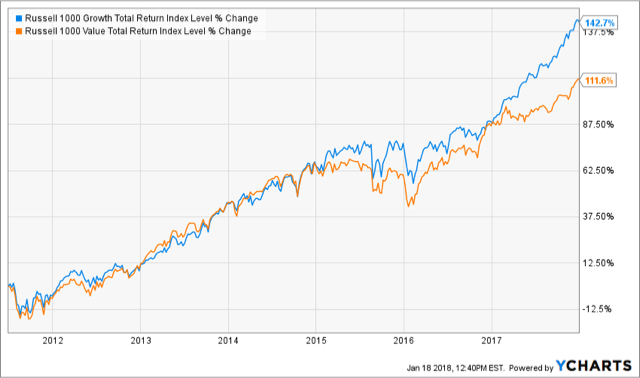

Wilson Capital’s commentary has often chronicled the exuberant growth stocks that have outperformed their value counterparts since the 2008 financial crisis. Since the beginning of 2017, this performance gap has widened considerably, as industries like bio-tech and information technology have soared while more staid industries like energy and consumer retail have lagged. This in itself is not a reason for caution, but could lead to issues if the expectations of future growth fail to materialize. The below charts illustrate the returns of Growth* and Value* stocks in the period during the 2000 tech bubble and the current market. While it is far too early and with the environment much changed than that of the 2000 tech bubble, the charts show an eerie similarity to the period preceding that eventual bubble pop as Growth stocks start to de-couple from Value stocks.

1995-2002

2011-2018

Source: YCharts

In addition to rising stock prices, the recent emergence of crypto-currencies such as Bitcoin does not suggest that investors are eager to be tethered to earth anytime soon. This new investable asset is literally a made-up form of currency without any monitoring authority that has less tangible worth than Monopoly money since it does not exist in physical form. A keen investor would keep an eye on the rationality of the public if the crypto-currency market continues higher.

Interest Rates

Over the course of the past 2 years, the U.S. Federal Reserve has increased the Federal Funds Rate* from its low of 0% up to 1.4% as of December 2017. In the aftermath of the 2008 financial crisis, the Federal Reserve went to drastic measures by lowering the rate to 0% in an effort to encourage lending which would lead to reduced unemployment rates and jumpstart the economy. With the unemployment rate now at pre-recession lows, the Fed is less concerned about rising unemployment but rather the prospect of over-heated markets with high inflation. To counter that possibility the Fed has begun the process of raising short-term interest rates. This policy works well within the confines of textbooks, but may not offer the exact remedy that economists predict. Issues can arise if the higher rates temper investment and the improved employment market reverses. It also raises the probability of a so-called “inverted yield curve” whereby the interest rates on the shortest term bonds (think of a savings account interest rate) equal or exceed those of the longest-term bonds with maturities of 30-years. In this rare phenomenon, investors are paid more to hold an investment with less risk. Along with breaking the traditional risk-to-reward trade, an inverted curve has been a precursor to recession 7 times since 1970.

Politics

With less than a week to go in 2017, the biggest change to taxation law in the United States since 1986 was passed in a hasty fashion in order to cap off President Trump’s first year in office. The bill was passed without any Democratic votes and Republicans promoted the bill as a tax cut to the middle class. In reality the meat of the bill deals with changes to the corporate tax code (that was viewed favorably from both parties) and includes only modest tax cuts to a vast majority of taxpayers. At the same time it is projected to add over $1 trillion to the federal deficit over the next 10 years. Despite many positive aspects, the lack of both input by the minority party and true reform to the tax code paints a dim picture of the current state of governance during the Trump Administration. While the markets have largely avoided the “noise” of the political environment as investors bask in the positive benefits corporations will enjoy from tax reform, there are fewer legislative levers left that can be pulled to benefit businesses. This all leads to the all-important mid-term elections this November which could prove to be a referendum on the Trump presidency.

Glossary

Growth – Stocks that are growing sales and earnings at a higher pace than other stocks. Investors are typically willing to pay a higher price for growth stocks, leaving them susceptible to sudden drops.

Value – Stocks that are cheaper on a per-share amount of sales or earnings. In many instances value stocks are former growth stocks that have reached maturity without a catalyst for future growth.

Federal Funds Rate – Interest rate used by the largest banks to lend money in the shortest time periods, usually overnight.

† Indices used to represent asset classes:

U.S. Large Cap Stocks – S&P 500

U.S. Small Cap Stocks – Russell 2000

International Stocks – MSCI ACWI ex-U.S.

U.S. Bonds – Barclays Aggregate

Commodities – Bloomberg Commodity

IMPORTANT INFORMATION

The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes and represents Wilson Capital’s views based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Wilson Capital is a Registered Investment Advisor (“RIA”), registered in the state of Massachusetts. Wilson Capital provides asset management and related services for clients nationally. Wilson Capital will file and maintain all applicable licenses as required by the state securities boards and/or the Securities and Exchange Commission (“SEC”), as applicable. Wilson Capital renders individualized responses to persons in a particular state only after complying with the state’s regulatory requirements, or pursuant to an applicable state exemption or exclusion.

Click here to download a printable PDF 4Q17-Investment-Letter.pdf (10972 downloads )